Subscription Plans

Invest in Your Edge

Self-directed ETF allocation intelligence for investors who want daily structure, market context, and disciplined rebalancing guidance.

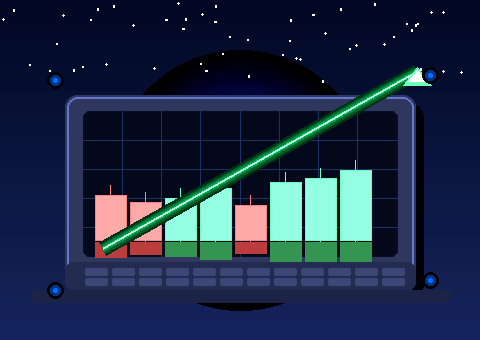

📈 3-YEAR BACKTEST · CALM GROWTH MODEL

$10,000 → $22,306

May 2023 → May 2026 · fees & slippage included

+123%

Total Return

+30%

Annualized

−4.75%

Max Drawdown

Subscription

$480/yr

signal paid for itself 25×

Simulated backtest — not actual trading results. Past performance does not guarantee future returns.

✅ START HERE — FREE

📧 Free

Newsletter & Market Forecast

$

0

/month

Free access — register once and unlock the Market Forecast, Backtest history, and weekly newsletter

- 📊 Daily Market Forecast — upcoming Market Opening weather forecast, by Quant Research Engine

- Backtest section access

- Weekly market newsletter

- BLEE research updates

- Daily signal page

- Email & SMS alerts

- Auto-trade tools

Instant access · No credit card

🔜 COMING SOON

⭐ Starter

Daily Signals

$

29

/month

or $290/year — save $58 (2 months free)

📈 IF YOU FOLLOWED OUR SIGNAL WITH $10,000

Invested

$10,000

→

3 years later

$22,306

+$12,306

+123%

Annualized +30% · Max drawdown −4.75% · vs S&P 500 +86%

Simulated backtest May 2023–2026. Past results ≠ future performance.

Simulated backtest May 2023–2026. Past results ≠ future performance.

Access to our dedicated Daily Distribution Signal — follow and grow your investment portfolio steadily, with lower risk than other investment products including the S&P 500, so you can sleep peacefully.

- Everything in Free

- Daily ETF allocation signal

- Portfolio performance tracker

- Historical backtest data (6 yr)

- Email & SMS alerts

- BLEETrader desktop app

- Auto-trade (Schwab/IBKR)

Want to be notified? Contact us →

🔜 COMING SOON

🚀 Pro

Brokerage Integration

$

49

/month

or $490/year — save $98 (2 months free)

Daily signals + BLEETrader app with 1 auto-trade investment model

- Everything in Starter

- Daily email signal alert

- Daily SMS signal alert

- BLEETrader desktop app (Win/Mac)

- 1 auto-trade investment model (Schwab/IBKR)

- You stay in full control

- Priority email support

We'll notify you when Pro launches